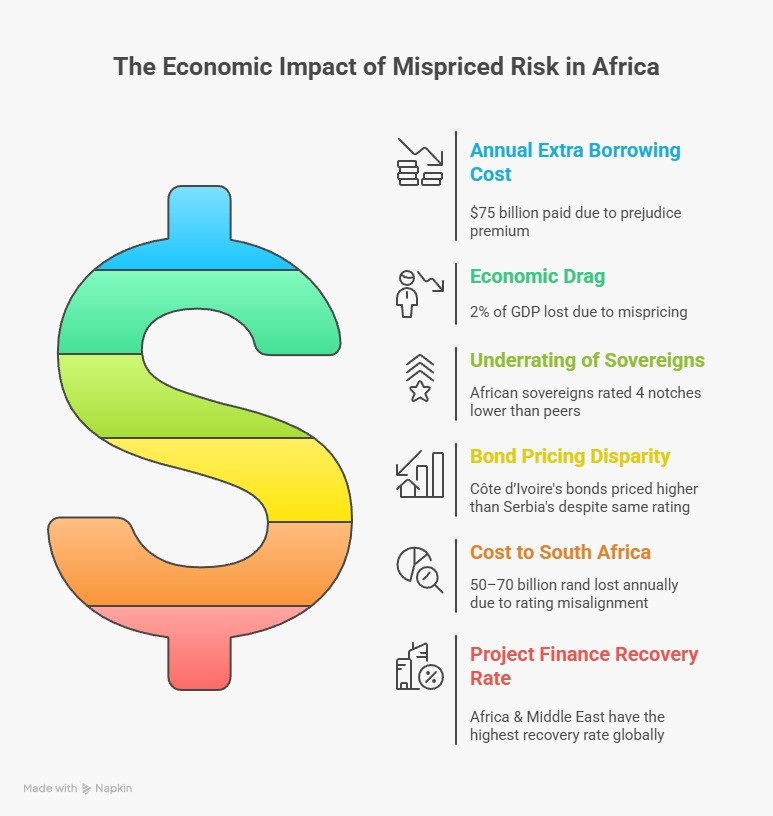

At the Bloomberg Africa Business Summit: November 17–18, 2025, in Johannesburg, South Africa, CEOs of the continent’s largest banks addressed one of the region’s most persistent economic barriers: the high cost of capital. The discussion opened with a stark statistic from the Africa Finance Corporation: African countries pay an estimated $75 billion annually in additional borrowing costs, a burden often described as the “prejudice premium.”

The Perception Tax on African Sovereigns

Stanbic CEO Sam Mkhwanazi described the pricing gap as “scandalous,” citing cases in which African sovereigns with similar credit profiles to peers in Europe or Eastern Europe face materially higher costs. He pointed to Côte d’Ivoire’s bonds trading 50 bps above Serbia’s, despite comparable ratings, and South Africa being rated four notches below where economic data suggests it should be.

This misalignment, he noted, wipes out roughly two percentage points of GDP across the continent.

While global rating agencies have increased their African presence—Moody’s acquisition of GCR and S&P’s expanded South African footprint—he argued that sovereigns still need to strengthen investor relations, increase transparency, and reinforce monetary policy independence to correct persistent mispricing.

Africa’s Responsibility: Mobilising Domestic Capital

Access Bank’s Roosevelt Ogbonna agreed but stressed that Africa must also confront its internal constraints. The continent is home to significant pools of capital—pension funds, institutional assets, and cash-rich sectors—that often remain idle or are invested offshore.

Ogbonna argued that Africa will continue to pay the premium as long as it relies heavily on foreign markets for sovereign borrowing. Mobilising domestic capital, he said, would create resilience, deepen local markets, and reduce dependency on external credit ratings that tend to overstate risk.

Both leaders emphasised that African issuers have strong repayment track records and high recovery rates, with global project finance in Africa and the Middle East recovering up to 85%, the highest worldwide.

Beyond Defaults: The Battle Against Perception

ABSA Group CEO Kenny Fihla added that the issue extends beyond sovereigns. Because banks’ credit ratings are directly tied to their home countries, the perception premium cascades through entire economies—affecting businesses, consumers, and intra-African trade.

He argued that correcting the perception gap requires Africa to tackle internal obstacles that raise transaction costs, complicate capital mobility, and weaken investor confidence.

Geopolitics, Markets, and the Trump Factor

The conversation shifted to geopolitics after comments made by U.S. President Donald Trump about potential military involvement in Nigeria. While initial market reaction was volatile, Nigeria proceeded with its Eurobond issuance—ultimately raising over $12 billion in demand for a $2 billion offer, far exceeding expectations.

Ogbonna noted that markets responded not to political noise but to fundamentals: Nigeria’s currency reforms, energy policy shifts, and clearer monetary policy signalling since 2023. The episode highlighted investors’ ability to look beyond short-term geopolitical rhetoric when long-term economic reforms are credible.

Amid Global Turbulence, Africa’s Outlook Brightens

South African executives noted that economic forecasts for the region have steadily improved over the year. The IMF now expects:

• South Africa to grow at 1.2%

• The African continent at approximately 4.5%

• Kenya, Tanzania, and Egypt around 5%

They highlighted the growing diplomatic engagement between Africa and the global south—China–Africa forums, Gulf–Africa deals, and renewed U.S. and EU engagement—as indicators that Africa remains central to global economic strategy.

A New Era: African Banks Filling the Gap

With several Western institutions scaling back operations across Africa, indigenous banks are expanding.

Ogbonna noted that Access Bank has absorbed businesses from banks like Standard Chartered, BNP Paribas, and Société Générale, which are exiting select markets due to shrinking margins and rising compliance costs.

African banks, he said, are more committed to offering full-service banking—retail, SME, corporate, and investment banking—rather than cherry-picking profitable segments. This deeper engagement allows them to drive local economic growth from within.

ABSA’s Strategic Pivot

Fihla confirmed that ABSA finalized its post-August strategic plan. The bank will:

• Reinforce client-focused differentiation across retail, business, and corporate banking.

• Reduce concentration risk by expanding outside South Africa into high-growth African markets.

• Accelerate modernization, improving efficiency and reducing cost-to-serve through technology transformation.

The strategy underscores a wider industry shift: African banks are increasingly regional, operationally leaner, and more aggressive in market expansion.

Thanks for reading, Daily Dive South Africa is an AI-powered news app delivering verified perspectives from multiple trusted sources in seconds.

We’re on a mission to help South Africans get the news that matters — smarter, faster, and free from AI misinformation.

🗞 Get the real situation, the smart way

📲 Download the app today.

📺Source: YouTube